American Consumers Being at Breaking Point Won’t End Well

U.S. consumers are at a breaking point, and that’s really bad news for the U.S. economy. It says that, despite all the rosy economic data we’ve been seeing lately, a severe slowdown is brewing.

Consumer spending is one of the biggest forces behind the U.S. economy. Look back at any previous economic slowdown in the U.S., and you’ll see that it was triggered by consumers.

In fact, it wouldn’t be wrong to say that the worse that consumers are doing, the more severe the slowdown will be for the U.S. economy.

On that note, there are three charts worth watching closely.

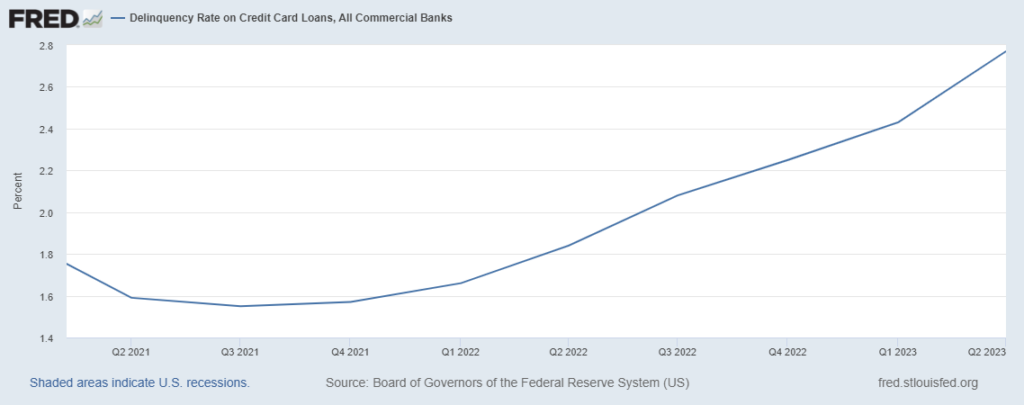

Consumers Having Hard Time Paying Credit Card Bills

The first chart worth watching is the delinquency rate on credit card loans at U.S. banks. Essentially, it tells us the percentage of credit card loans that are in bad shape (i.e., consumers aren’t paying them back).

As of this writing, the U.S. credit card loan delinquency rate is 2.77%.

That percentage might seem low, but it has risen to multiyear highs very quickly. In the third quarter of 2021, the delinquency rate on credit card loans in the U.S. was at record low levels. The last time the rate was as high as it is now was back in 2012!

(Source: “Delinquency Rate on Credit Card Loans, All Commercial Banks,” Federal Reserve Bank of St. Louis, last accessed November 15, 2023.)

U.S. Saving Rate Tumbles

The second chart worth watching is the U.S. personal saving rate chart. This rate is the percentage of disposable income that consumers have been saving.

The U.S. saving rate has really tumbled lately. In mid-2021, Americans were saving more than 12% of their disposable income. As of September 2023, the U.S. personal saving rate was just 3.4%, representing a decline of 71%.

(Source: “Personal Saving Rate,” Federal Reserve Bank of St. Louis, last accessed November 15, 2023.)

You know what’s really worth noting? Given that interest rates are currently high, Americans can actually generate decent returns on their savings, but they aren’t saving their money. Could it be because they’re struggling to keep up with the rising costs of living?

The saving rate tumbling shouldn’t be taken lightly. It means future consumer spending might not be as high as before, which wouldn’t be good for the U.S. economy.

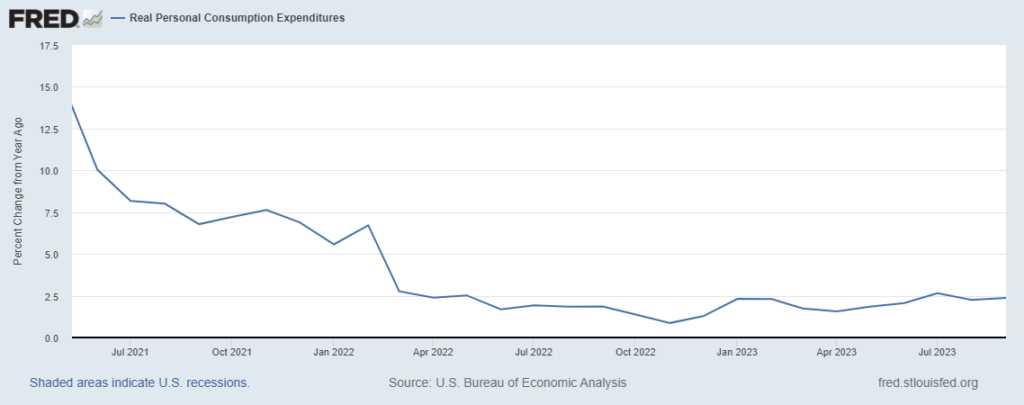

Consumption Rate Decelerating at Alarming Pace

The third chart worth watching is the one for real personal consumption expenditures. This gives us a peek into how much U.S. consumers are spending.

The following chart plots the year-over-year change in U.S. consumption spending (adjusted for inflation).

See the trend?

Surely, consumption has been growing lately, but the pace of the growth has really dropped. In mid-2021, U.S. consumption expenditures increased at a rate of close to 15%. Recently, they’ve been growing at just 2.4%. This is a big decline, and it makes the case for U.S. consumers being at a breaking point much stronger.

(Source: “Real Personal Consumption Expenditures,” Federal Reserve Bank of St. Louis, last accessed November 15, 2023.)

U.S. Economy Headed Toward a Slowdown: What Investors Need to Know

Dear reader, the above three charts are just a few of many indicators suggesting that consumers in the U.S. economy are at a breaking point. This won’t end well. If history tells us anything, a severe economic slowdown could be around the corner.

What I find comical is that there’s still an idea floating around that the economy is headed toward a soft landing, or even no landing. Have mainstream economists stopped looking at the data?

For investors, the suffering of American consumers has negative impacts on many industries and sectors. If the conditions get worse, there could be severe consequences.

For instance, if consumers run out of money, will they buy bigger homes, newer cars, and cooler gadgets? It’s very unlikely, and this could have a negative impact on the earnings—and eventually, the stock prices—of companies that sell big-ticket items.