Mortgage Rates Spiking, Housing Market in Danger Zone

Ominous clouds could be gathering over the U.S. housing market. Investors beware!

While the experts have been busy trying to figure out what the Federal Reserve is going to do with interest rates, they’ve been paying very little attention to the U.S. housing market.

The market is in dangerous territory, and it could be just a matter of time before we see falling home prices (and the economic mess that comes with it).

Here’s some perspective.

The U.S. housing market is highly correlated with mortgage rates. Low mortgage rates mean higher housing demand and, eventually, higher home prices. In contrast, high mortgage rates mean lower demand for housing and, eventually, lower home prices.

In the U.S., home prices haven’t come down much, but that could be the next shoe to drop. So far, we’ve seen the deceleration of home price increases in the U.S., but haven’t witnessed outright declines.

From 2021 to late 2022, mortgage rates were creeping higher. Since late 2022, they’ve been moving sideways but are still much higher than where they were after the 2008/2009 global financial crisis.

What does this mean? At their core, the higher mortgage rates mean an eventual slowdown of the U.S. housing market.

(Source: “30-Year Fixed Rate Mortgage Average in the United States,” Federal Reserve Bank of St. Louis, last accessed April 30, 2024.)

Cracks Appear in U.S. Housing Market

Some cracks have already been showing up in the housing market.

For instance, take a look at existing home sales. These are sales of already-built homes.

In March, the seasonally adjusted annual pace of existing home sales in the U.S. was 4.19 million units. That was down by 4.3% month-over-month and 3.7% year-over-year. (Source: “Existing-Home Sales Descended 4.3% in March,” National Association of Realtors, April 18, 2024.)

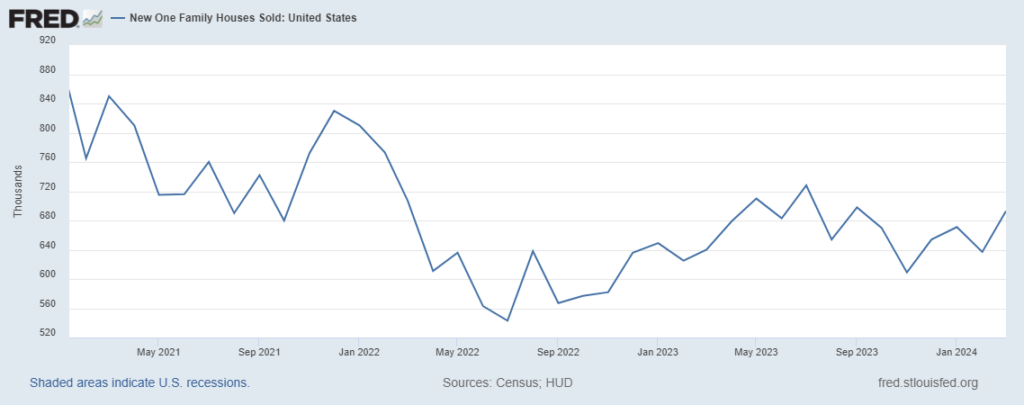

New home sales in the U.S. have also been declining (as the following chart shows). In March 2021, the seasonally adjusted annual pace of new single-family home sales in the U.S. was around 850,000 units. In March 2024, the pace was 693,000 units. This represents a decline of close to 20%.

(Source: “New One Family Houses Sold: United States,” Federal Reserve Bank of St. Louis, last accessed April 30, 2024.)

Regarding the slowdown in housing market activity, the chief economist at the National Association of Realtors, Lawrence Yun, said, “Though rebounding from cyclical lows, home sales are stuck because interest rates have not made any major moves.” (Source: National Association of Realtors, April 18, 2024, op. cit.)

What if the U.S. Housing Market Goes Down?

Dear reader, I’m not trying to scare you here, but it’s critical to know what’s going on with the U.S. housing market. The problems don’t stop with home prices going down; they could cause significant consequences across the board.

The U.S. housing market provides a major windfall to the U.S. gross domestic product (GDP). More activity in the housing market means more jobs and the flourishing of more ancillary industries. For example, more housing being sold could mean higher sales of furniture, appliances, lawn mowers, etc.

But that’s not all. If you’re an investor, your portfolio could be on the line.

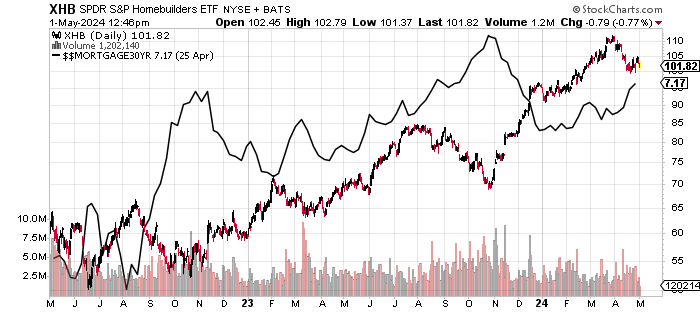

Consider home builder stocks. They’ve seen a robust move to the upside as mortgage rates have increased and housing activity has become anemic. Odd.

Chart courtesy of Stockcharts.com

Home builder stocks could get hurt as the U.S. housing market suffers.

Lastly, the mortgage market in the U.S. is huge. If home prices suffer, there could be stress on mortgages. Those who own mortgages could face severe losses, and the financial system could get bruised.