U.S. Economy Starting to Show Cracks

Stagflation in the U.S. economy could be a likely scenario in the coming quarters. Investors should be careful because stagflation is the worst of both worlds and makes investing very difficult.

Before going into any details, what is stagflation? In simple terms, it’s when there’s slow economic growth, higher unemployment, and persistent inflation at the same time.

Here’s some perspective on why the case for stagflation in the U.S. economy is getting stronger.

The U.S. economy is starting to crack. The vast majority of U.S. gross domestic product (GDP) is based on consumption, and it’s starting to look like consumption could be getting hurt. If U.S. consumption goes down, so will the U.S. economy.

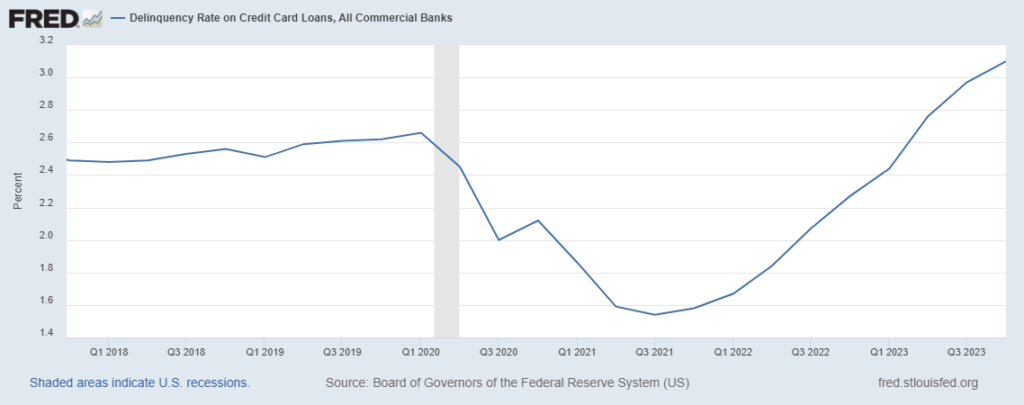

U.S. consumers are starting show signs of financial stress. Take a look at the chart below; it plots the U.S. delinquency rate for credit card loans at all commercial banks.

In the first quarter of 2022, the delinquency rate for credit card loans was around 1.67%. At the end of the fourth quarter of 2023, the rate was 3.1%, which was more than a decade high. Worth noting is that the credit card delinquency rate rose to more than a decade high in just a few quarters.

If this trend continues, will consumers go out and spend? It’s unlikely.

(Source: “Delinquency Rate on Credit Card Loans, All Commercial Banks,” Federal Reserve Bank of St. Louis, last accessed May 7, 2024.)

But that isn’t all.

Recently in the U.S., the housing market has been slowing, the rate of construction growth has also been slowing, retail sales have been stagnating, the personal saving rate has been dismal, and the list goes on.

Job Cuts Growing & Hiring Isn’t

Now, what’s been happening on the employment front? It’s not looking good.

Take a look at the April 2024 “Challenger Report,” which is issued by Challenger, Gray & Christmas, Inc., a global outplacement and business and executive coaching firm. The company’s monthly report tracks the number of job cuts announced by U.S.-based firms.

Year-to-date (as of the end of April), U.S. companies announced 322,043 job cuts. Moreover, the amount of time it takes to find a job in the U.S. has been increasing. The average job search lasted 3.05 months in the first quarter 2024. That’s compared to 2.71 months in the first quarter of 2023. (Source: “April 2024 Job Cuts Announced by US-Based Companies Fall; More Cuts Attributed to TX DEI Law, AI in April,” Challenger, Gray & Christmas, Inc., May 2, 2024.)

Hiring numbers haven’t been looking good, either. In the first four months of 2024, U.S. employers announced plans to hire 46,597 workers. This is a lower total for the first four months of a year since 2016!

U.S. Inflation Has Been Sticky

Lastly, when it comes to inflation, it’s been sticky.

Certainly, the rate of inflation in the U.S. economy has come down lately, but it remains above the range that the Federal Reserve has been targeting: between two and three percent.

In the first three months of 2024, the Consumer Price Index (CPI)—an official measure of inflation at the consumer level—increased by 1.1%. (Source: “Consumer Price Index for All Urban Consumers (CPI-U),” U.S. Bureau of Labor Statistics, accessed May 7, 2024.)

Assuming this pace continues, the annual rate of inflation in the U.S. for 2024 could end up being well over four percent!

What to Do if Stagflation Takes Control

Dear reader, as I said earlier, the case for stagflation in the U.S. continues to get stronger.

In a recent press conference, the Fed’s chairman, Jerome Powell, hinted that he doesn’t see any stagflation. But don’t take those words too seriously. We could very well be in the early stages of stagflation, just not full-blown stagflation. The Fed will eventually come to terms with it and call it what it is.

Note that the Fed was very wrong about how long higher-than-normal inflation would stick around.

For investors, stagflation is the worst of both worlds: a slowing economy at the same time as higher inflation.

In times of stagflation, being defensive can pay, versus being aggressive. Growth stocks and consumer discretionary plays could get hurt badly. Meanwhile, gold, utilities, and consumer staples could outperform the overall market.