U.S. Housing Market Showing Signs of Severe Stress

There’s one sector that shouldn’t be ignored by investors: the U.S. housing market. There are fundamental problems that tell us there could be a rough patch ahead for the housing market. Home prices could fall further, and homebuilders and related companies could face severe headwinds.

Before going into any details, here’s an overview of how the U.S. housing market looks at the moment.

U.S. home sales have been falling like a rock.

In January of this year, there were 670,000 new single-family home sales in the U.S. In January 2022, there were 831,000 new single-family home sales. In January 2021, there were 911,000 such sales. This represents a one-year decline of 19.4% and a two-year decline of 26.5%. (Source: “New One Family Houses Sold: United States,” Federal Reserve Bank of St. Louis, last accessed March 8, 2023.)

Existing home sales (sales of already-built homes) have been falling especially hard in the U.S. In January, there were 4.0 million existing home sales in the country. In January 2022, there were more than 6.3 million existing home sales. This represents a decline of close to 37% in just one year. (Source: “Existing Home Sales,” Federal Reserve Bank of St. Louis, last accessed March 8, 2023.)

Home prices have also been tumbling. In June 2022, the S&P/Case-Shiller U.S. National Home Price Index stood at 308.4. In December 2022, it was at 294.7. This represents a decline of more than four percent in six months. (Source: “S&P/Case-Shiller U.S. National Home Price Index,” Federal Reserve Bank of St. Louis, last accessed March 8, 2023.)

The S&P/Case-Shiller U.S. National Home Price Index is one of the best measures of home price trends in the U.S. Note that the index, which is calculated using the three-month moving average of U.S. residential home prices, has a two-month lag.

Rising Interest Rates

Interest rates act as a gravitational pull for the housing market. The higher the mortgage rates, the fiercer the gravity in the housing market. Simplifying this further, the higher the interest rates, the lower the affordability of—and, subsequently, the demand for—home purchases.

Take a look at the chart below. It plots the 30-year fixed mortgage rate in the U.S.

As the Federal Reserve has tried to curb inflation in the U.S. economy, it has raised its benchmark interest rate. This has led mortgage rates in the U.S. to also rise. In 2021, the 30-year fixed mortgage rate was around 2.75%. Now, it’s close to seven percent. This is an increase of about 150%.

Chart courtesy of StockCharts.com

Recently, the chairman of the Federal Reserve said central banks could raise interest rates further. This would be nothing but bad news for the U.S. housing market. Soaring interest rates could take a further toll on the housing market. The longer mortgage rates stay high, the lower the demand for—and prices of—homes will get.

Irrationality Among Stock Investors

As it stands, I see a disparity between the fundamentals of the U.S. housing market and how investors are pricing the stocks of homebuilders and related companies.

With the data for the U.S. housing market looking dismal already, and its outlook being anemic, you might assume that companies that rely on the housing market have been performing horribly. How can they be making money if home prices and sales have been plummeting?

Investors might be completely disregarding the fundamentals of those companies.

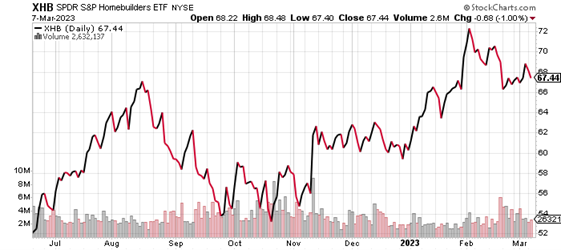

Take a look at the chart below of the SPDR S&P Homebuilders ETF (NYSEARCA:XHB), an exchange-traded fund (ETF) that tracks the performance of homebuilder stocks. Despite the poor housing market, the ETF’s performance has been robust lately.

Chart courtesy of StockCharts.com

What’s Ahead for Home Prices & the U.S. Housing Market in 2023?

Dear reader, as interest rates remain high and the demand for housing purchases slumps, could homebuilders and related companies continue to perform well? For investors who own a lot of these stocks, it could be time to pause and reflect.

Furthermore, homes are sometimes retirement assets for Americans. As home prices go down, it could really dampen Americans’ financial sentiment and affect the way they spend their money. Don’t forget, consumers are a major force in the U.S. economy.

The U.S. housing market is currently walking a very fine line. Investors might be ignoring the risks that are brewing, but being complacent at this time could be a bad idea.