S&P 500 on a Comeback?

There has been a lot of talk about how the latest first quarter results show that the S&P 500 and broader stock market is on a comeback, which is a little funny on the surface since the S&P 500 is trading near record levels. What is it making a comeback from?

If anything, investors could point to the 2017 first quarter results as justification for the sky-high valuations, but even that is a little off the mark. The first-quarter results for 2017 do not in fact suggest the S&P 500 is on a comeback. If anything, the results further illustrate how susceptible the stock market is to a serious correction or stock market crash in the coming months.

Advertisement

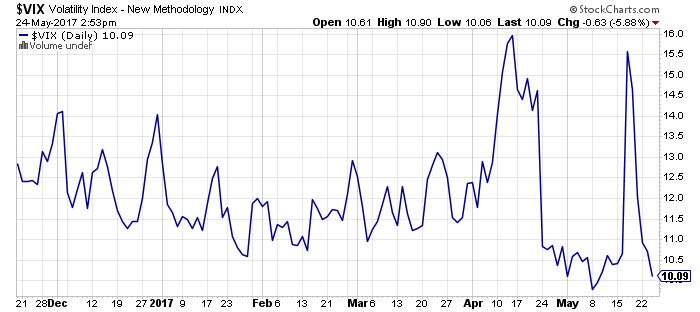

Despite chaos within the Trump administration and gridlock in Washington, the S&P 500, Nasdaq, and Dow Jones Industrial Average are all near record levels. Meanwhile, investor complacency, as gauged by the CBOE Volatility Index (VIX) is at its lowest levels since the Financial Crisis.

The VIX, better known as the “fear index,” measures market volatility; the higher investors expect the S&P 500 to fluctuate, the higher the VIX goes up. The VIX spiked on Wednesday, May 17, on fears that President Trump’s firing of FBI Director James Comey could be the first step in a long walk to impeachment. But investors shrugged off those concerns and the VIX returned to its near-decade low.

Chart courtesy of StockCharts.com

At a time when stock valuations are at nosebleed levels, political tensions in Washington are soaring, and geopolitical tensions around the world are simmering, investor complacency reigns supreme.

Why? Investor optimism is being buoyed by so-called strong first-quarter results. After a record five-quarter earnings recession, S&P 500 profits have improved over the last three quarters. Voila, the U.S. economy is doing well as are corporate earnings!

And by extension, so is the stock market. After all, investors tend to reward stocks more than any other time when companies report strong earnings growth. That said, investors also rewarded stocks during the heady days of quantitative easing for not losing as much money as they thought they would. This might explain why it’s been win-win for the S&P 500 since the markets bottomed in March 2009.

Anyway, the strong first quarter results are (apparently) encouraging because they come even before Trump gets his tax cuts and stimulus spending going. Imagine how healthy the U.S. economy and strong corporate profits will be when Trump finally gets his campaign pledges enacted?

Corporate Earnings Growing at Fastest Pace in 6 Years?

Everything is relative. This might explain why Wall Street can crown 2017’s first-quarter earnings as experiencing the fastest growth in six years. First quarter earnings for companies in the S&P 500 advanced approximately 14% on a year-over-year basis. This also represents the biggest increase since the third quarter of 2011.

Looking ahead, Wall Street believes the current double-digit earnings growth will continue…despite weak U.S. economic data and anemic gross domestic product (GDP) growth. Analysts are predicting a 10% increase in earnings for S&P 500 companies in all of 2017. In 2018, analysts expect S&P 500 companies to report a 12% increase in earnings.

While all of this is encouraging to say the least, and helps analysts justify stock market valuations that are in the stratosphere, 2017 first quarter earnings are not nearly as good as they appear. And the notion of a stock market crash is not as outlandish as it seems.

Earnings Recession Over

Everything looks good from the bottom. In fact, on a year-over-year basis, it looked like earnings had nowhere to go but up. A year ago, the S&P 500 was in the middle of its longest earnings recession.

Fast forward to 2017, and the S&P 500 is out of an earnings recession, which is obviously a good thing. Unfortunately, the strong growth is not a result of the U.S. economy, it comes in spite of the U.S. economy.

U.S. Economy Hindering Corporate Earnings

In the first quarter of 2017, S&P 500 companies that get more than half their sales from outside the U.S. reported average EPS growth of 20.9%. S&P 500 companies that rely on the U.S. for the majority of their revenue reported average first-quarter EPS growth of just 9.9%. (Source: “Earnings Insight,” FactSet Research Systems Inc., May 12, 2017.)

Financial Engineering

Second, more and more companies are relying on financial engineering to make their financial results look decent. This is a tried and true throwback to the Financial Crisis, when corporate America relied on share buybacks, streamlining, and non-GAAP (generally accepted accounting principles) data to make their results look better than they really were. Earnings and revenues are down, but thanks to some creative accounting, earnings are up!

More and more companies are reporting adjusted earnings that make corporate profits appear better than they really are. All publicly traded companies in the U.S. report EPS on a GAAP basis, but many also report EPS on a non-GAAP basis. The argument being that non-GAAP EPS information provides investors with a more accurate picture of a company’s daily operations because it excludes short-term, one-time events that hurt profitability.

Because there is no standard of what qualifies for exclusion in non-GAAP EPS, corporations are able to manipulate and boost their non-GAAP EPS. And frankly, many investors do not know the difference between GAAP and non-GAAP EPS. They just look at the numbers.

In the first quarter, 19 (63%) of the 30 companies in the Dow Jones reported both GAAP and non-GAAP EPS. Of these 19 companies, 15 (79%) reported non-GAAP EPS that beat their GAAP EPS. (Source: “Earnings Insight,” FactSet Research Systems Inc., May 19, 2017.)

S&P 500 Is a Two Trick Pony

Investors can champion an S&P 500 comeback when stocks experience broad-based growth. But that isn’t happening. The Energy sector, thanks to a rise in oil prices, was the leader for both year-over-year earnings growth and revenue growth.

In the first quarter of 2016, the Energy sector reported a loss of $1.5 billion. In the first quarter of 2017, the Energy sector reported earnings of $8.5 billion. Remove the Energy sector from first-quarter 2017 results and the blended earnings growth rate for the other 10 sectors plunges from 13.9% to 9.7%.

Banks also did well in the first quarter, jumping nearly 20% on a year-over-year basis with four of the five industries in the sector reporting growth; all of which were double-digit earnings growth. Remove financials from first quarter 2017 results and the S&P 500 advanced seven percent; far better than the first quarter of 2016 but not nearly as good as it appears.

Corporate profits are up, but they aren’t exactly rebounding like first quarter 2017 data suggests. The numbers look strong, but corporate profits are growing much slower than they were a few years ago. As a result, the champagne kisses and caviar dreams of an economic and corporate rebound are a little premature. Talk about a stock market crash though is not so premature.

And the positive outlook for full-year 2017 EPS growth of 10% and 2018 EPS growth of 12% will still only achieve a five-year average annual increase of between four and six percent. The P/E ratio for the S&P 500 is currently at 23.44, basically even from 23.49 from a year ago and significantly above the 18.41 estimate for the full-year. (Source: “Market Data Center,” The Wall Street Journal, last accessed May 24, 2017.)

It’s going to take more than just a quarter or two of earnings growth to justify the current S&P 500 valuations. If Trump is not able to deliver on his economic promises, the Trump Bump rally could come to a crashing end. If Trump is stymied by political turmoil in Washington and his tax cuts are postponed until 2018, the current bull market will experience a major correction or even a stock market crash.

Talks of impeachment would crush the stock market as well. Investors will be more than a little reluctant to buy shares and keep the current long-in-the-tooth bull market running in the midst of the economic and political uncertainty that arises from a presidential impeachment.

Corporate earnings are not as strong as they appear and the U.S. economy is not as responsible for the decent first-quarter results as investors think. The U.S. economy remains weak, and if Trump can’t get his economic policies passed, it will be tough for Trump to drive U.S. GDP growth, from last year’s abysmal 1.6%, to a sustainable three to four percent. It could also mean the Federal Reserve will step in and actually cut its key lending rate; not something that would look good for the great economic negotiator.

Without this economic driver and investor optimism, it will be impossible to justify the current levels of the S&P 500…no matter what kind of earnings S&P 500 companies throw up in the second, third, and fourth quarters of 2017.