Jamie Dimon Sees Many Obstacles to Robust Growth, Implying Future Financial Crisis

Jamie Dimon is not pleased. The financier with a 10-digit net worth is worried obstacles in the economy will prevent it from reaching its true potential. If true, this greatly raises the odds of a future financial crisis, as America cannot meet its obligations without robust growth (three-percent-plus annually, in perpetuum). This will soon enough bring to heel entitlement spending and every other public service the government spends funds on. The results won’t be pretty for large segments of society.

According to Dimon, a confluence of factors are threatening to torpedo future growth before it even starts. Many of these are apparent to those of us paying attention. Lack of tax reform, onerous regulations, and downright poor labor force data paint a picture of stagnation. “I think America has got to get its act together about a bunch of stuff, not just one.” (Source: “Jamie Dimon: ‘America has to get its act together’,” CNBC, June 7, 2017.)

Advertisement

Also Read:

The Analyst Who Nailed the 2008 Financial Crisis Has a New Warning

“Economic Crash 2017” and How Next Financial Crisis Could Be Worse than 2008

Let’s start with the sorry state of the future labor force. Data presented by Dimon provides quite the dystopian worldview. A full 70% of young men do not qualify for military service, because they can’t read, write, or are in poor health (suffering from largely preventable diseases like Type 2 diabetes). Half of high school students don’t graduate, and the ones that do, according to Dimon, are “not able to work a proper job.” Finally, labor force participation has dropped to 30-year lows (62.7%), with the younger demographic dropping fastest. (Source: Ibid.)

Dimon’s statistics are not only accurate, they’re just the tip of the iceberg. According to the Program for International Student Assessment (PISA), the U.S. ranks 40th in the world for math literacy. The U.S. could only muster a 25th-place ranking in science literacy and 24th in reading literacy. 29% failed basic baseline levels in math. (Source: “On the world stage, U.S. students fall behind,” The Washington Post, December 6, 2016.)

Why are these issues so important? Because it will be up to the next generation of American workers to stave off future financial crisis by becoming more productive and participating at greater rates for the economy to reach its true potential. It’s not coming from our existing aging and increasing unproductive labor force.

Future living standards of American retirees literally rest on the backs of those entering the workforce right now. For major business CEOs like Jamie Dimon to express this concern openly, they surely must be worried about the imminent competitiveness of their businesses. This doesn’t sound like robust growth is around the corner.

Regarding growth-stifling over regulation, Dimon had some choice words as well. He unloaded on America’s onerous regulatory environment, blaming it for the lackluster startups in new business formation. According to the data we’ve seen, he certainly has a point.

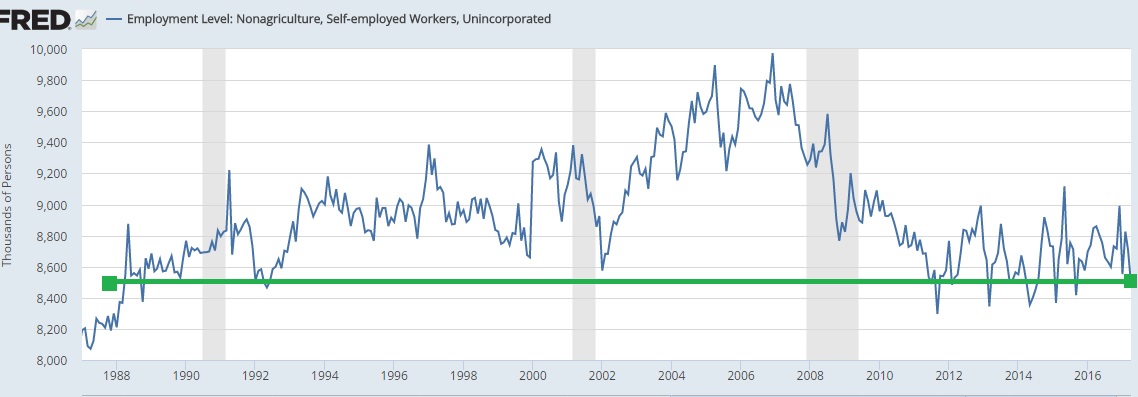

The Federal Bank of St. Louis has put out new numbers indicating the slow-motion collapse of the self-employed. America had as many self-employed people in 1988 as it does today (approximately 8.5 million people). If we account for the fact that population has increased 32% since 1988, today’s America should have over 11 million self-employed people, not 8.5 million. This is problematic since the self-employed are often the people who stimulate small-business creation—the lifeblood of America.

Fewer small business formations also has negative downstream effects for the financial services sector (which is why Dimon is so concerned). Fewer up-and-coming businesses means fewer financings and loans, which banks need to thrive in a low interest rate environment. Further downstream: lower tax receipts to government coffers because small business generally don’t have the means to repatriate earnings offshore. Lower growth is the net result, leading to future financial crisis.

Ultimately, the fact that Dimon is publicly professing his disappointment in the U.S. economy 2017 is troubling. A noted optimist and staunch believer in American exceptionalism, Dimon is obviously dissatisfied with the way trends are pointing. It’s not like these gripes carry “quick fix” potential either. These problems are long-term and will take many years of dedication to turn around—assuming the political will to solve them even exists.

Unfortunately, America doesn’t have enough time to let things play out. Without consistent three-percent or better growth, a “Japanification” of the economy will continue to spread. That will entail lower business cycle highs (low growth), frequent bouts of disinflation, increasing budget deficits, and a zombiefication of the private sector. Higher tax burdens will be thrust on populations to appease a revenue-starved government (all levels). Similar to the boiling frog scenario, life will get a little more difficult month-by-month, year-by-year.

And there’s not a darn thing the Federal Reserve can do about it. They’ve already thrown everything at the economy to jump start growth. They’ve lowered interest rates to nothing, they’ve shoveled money into the banking system, both foreign and domestic. They’ve even expanded the monetary base exponentially to get the velocity of money moving again. The only thing this accomplished was raising asset prices to bubble-like levels, and perhaps providing a short-term boost in consumption.

Although Jamie Dimon never said a future financial crisis is brewing, if we read between the lines, that’s exactly what he said. This should make every investor shudder in regards to what’s coming.

Worrying Trends in Consumer Credit

The labor force side of the economy is inextricably linked to consumer spending—that’s a fact. Higher economic growth and low unemployment should support higher wages, discretionary spending, and credit usage. But things aren’t turning out that way.

Jamie Dimon confirmed this view by lamenting the inability of homeowners to obtain mortgages. Quite a troubling statement with interest rates still near all-time lows and aggregate credit scores at the highest levels since the U.S. Housing crisis. Yet more data confirms this disturbing fact.

The Federal Reserve has released April 2017 numbers showing consumer credit in free fall. For starters, total credit issuance only rose $8.2 billion versus the $15.5 billion expected. This was the lowest monthly increase since August 2011. More troubling: non-revolving consumer credit fell sharply, indicating that fewer people are taking on important debt, like mortgages and car loans. (Source: “Consumers Hit The Brakes: Smallest Increase In Consumer Credit In 6 Years,” Zero Hedge, June 7, 2017.)

The ramifications for an economy deeply reliant on borrowing are clear. Without a large, steady, and sustained pick-up in non-revolving credit, a future financial crisis is assured. The morass of low growth will remain, along with all the unappealing side effects we’ve discussed. This also shows consumers are becoming timid to take on more debt, which is quite contrary to what usually happens at this point on a mature business cycle. Just imagine what those numbers will look like if Uncle Sam slides into recession.

Maybe Dimon is on to something.

Credits: Flickr.com/Daniel Rubio

What This Means for Asset Prices

Active investing is hard. What seem like logical places to take profits often occur way too early. Overvalued stock markets defy gravity, and grind ever higher. Devastating economic numbers proving earnings growth is finished is brushed aside in effortless fashion. Black is white, truth are lies, tyranny is freedom; in other words, absolutely nothing makes sense. Little wonder why some investors think this time is different.

But it never is. Important figures like Jamie Dimon wouldn’t be professing such concerns publicly if it were. Investors tend to forget that the topping action at the end of major stock market expansions can take years, not weeks or months. The melt-up we’re seeing this time around is an added twist, but it’s really the byproduct of several factors which aren’t sustainable. If this pervasive overvaluation was happening in a rising-earnings environment, or at the cusp of breakout growth, perhaps we’d understand. But the opposite is occurring and even the market bulls have run out of explanations.

If America ultimately falls into deflation’s death trap, stock prices and risk assets in general can crater. Look no further than the Nikkei 225 Index performance post-1989 to alleviate any doubts. The exchange fell 70% within a three-year span. An overheating economy and epic property bubble were the overvaluation catalysts on the way up, but the deflation that followed hollowed out their whole economy. The effects of the crash still persist today.

Present-day conditions in America are not similar. We’ve already experienced the property bubble a decade ago, and economists can only dream of the “problem” of an overheating economy. But the extreme valuations which pocked the Nikkei 225 exist, as does the deflationary threat to blow it all up. It’s not difficult to imagine what path the stock markets take if policymakers are unable to re-stimulate growth. Future financial crisis will morph into a present-day one.

The bottom line is, to stay invested in this market, one must believe this time is different. When you boil it all down, either stock market valuations will continue to expand, or the market will eventually succumb to the notion that rapid growth isn’t coming back, and re-price accordingly. That is, unless you believe breakout growth is just around the corner—a false narrative that has been pushed for the last seven years.

If there’s any confusion, just listen to the words of Jamie Dimon. That’s as explicit as it gets without being explicit.